UBM Plc has announced results for the year ending 31st December 2013

For full details and financial notes, click here.

- Revenues from continuing operations up 3.2% to £793.9m; organic revenue growth of 3.7%

- Adjusted operating profit from continuing operations up 6.3% to £186.3m; margin of 23.5%

- Continuing fully diluted adjusted EPS up 12.8% to 53.6p

- Total China revenues up 21% to £174.8m from £144.5m with strong annual and biennial event performance

- Events organic revenue growth of 6.3%; operating profit, up to £148.9m, margin of 32.2%

- PR Newswire 1.9% underlying growth and 22.6% margin

- £22.7m exceptional charges reflect Marketing Services restructuring and the implementation of new UBM-wide finance and reporting system

- Final dividend of 20.5p proposed; total 2013 dividend of 27.2p (2012:26.7p), up 1.9%

- Leverage improved to 2.2x Net Debt/ EBITDA (2012: 2.5x)

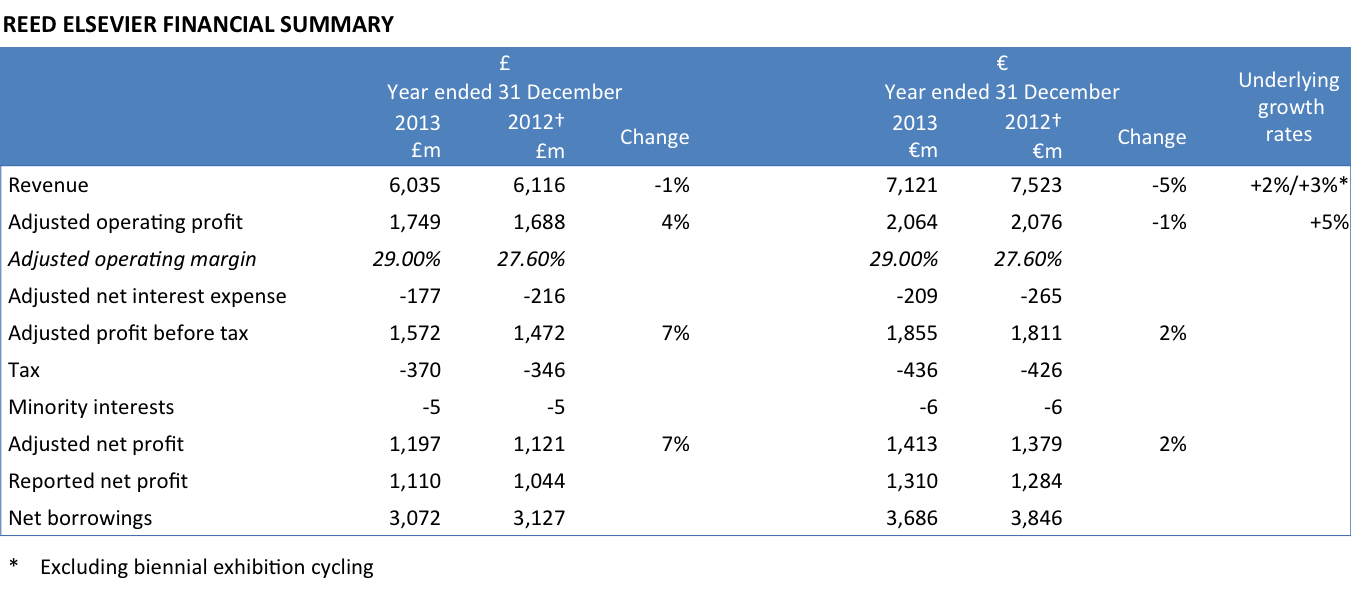

Click on the table for an enlarged view

Click on the table for an enlarged view

David Levin, UBM’s Chief Executive Officer, commented:

“2013 was a year of strategic progress and operational achievement for UBM against a difficult economic backdrop; the company can look forward to 2014 with confidence.

2013’s good revenue and profit growth was bolstered by a strong performance from our biennial events in the second half of the year. PR Newswire had a solid year in its core business and maintained its strong profitability. We disposed of our Data Services business and substantially restructured our Marketing Services activities to focus on the professional communities our events serve. We end the year with significantly higher quality earnings and with the business better positioned for structural growth.

Our strategy to develop UBM as an events-led marketing services and communications business is proving successful. The growing strength of our Events business — focused particularly on large events, and our strong presence in China and other growth markets — continues to affirm our strategic choices and to demonstrate live media is an increasingly significant component of business to business marketing programmes. PR Newswire has retained its leading, premium position in the online news and content distribution market, and is well placed to prosper in the emerging world of digital content marketing.”

UK, London

Related Articles:

- Progressive Digital Media Group acquires Pyramid Research from UBM Posted on December 12, 2013

- UBM plc sells Property Week to Metropolis and UBM Channel to The Channel Company Posted on September 27, 2013

- Mash Media acquires International Confex from UBM Live Posted on September 21, 2013

- David Levin to step down as CEO of UBM Posted on September 16, 2013

- UBM report a decline in profits for the first six months Posted on August 5, 2013

- UBM Asia to acquire NOVOMANIA in China Posted on March 7, 2013

- UBM results for the year ended 31 December 2012 Posted on March 1, 2013

- Electra Partners to acquire UBM’s Data Services businesses Posted on February 5, 2013

- UBM acquires outstanding 50% stake of Canada Newswire for £30.1m Posted on November 1, 2012

- UBM acquires 70% stake in Turkish baby product tradeshow EFEM Posted on October 18, 2012

- UBM – results for the six months ended 30 June 2012 Posted on July 30, 2012

- UBM Aviation Routes Limited acquires Airlineroute.net Posted on May 20, 2012

- UBM plc acquires Negocios nos Trilhos, South America’s leading railway industry exhibition Posted on April 16, 2012

- UBM 2011 results Posted onFebruary 28, 2012

- UBM acquires four tradeshows Posted on February 28, 2012

- UBM acquires Renewable Energy India Posted on February 28, 2012

- UBM plc acquires 4G World exhibition and conference Posted on February 7, 2012

- UBM sells its Daltons business Posted on February 7

- Founders of Briefing Media to acquire UBM’s UK agriculture and medical general practitioner portfolios Posted on February 7, 2012

- UBM plc and Roularta Media Group form Belgian medical print journal joint venture business Posted on February 3, 2012

- UBM TechWeb acquires Online Marketing Summit Posted on November 19, 2011

- Intent Media acquires UBM titles for £2.4m Posted on June 27, 2011

- UBM acquires 70% of US catering tradeshow business Catersource for $5 million Posted on June 21, 2011

- UBM plc acquires AMB exhibitions business in South East Asia Posted on May 12, 2011

- UBM Medica sells The Consultant Print Group April 29, 2011

- UBM Q1 results Posted on April 21, 2011

- UBM disposes of French medical print business Posted on March 1, 2011

- UBM disposes of UK licensed trade portfolio Posted on March 1, 2011

- UBM acquires Indian travel tradeshow SATTE Posted on March 1, 2011

- UBM to acquire stake in Famdent, India’s largest dental exhibition and conference business Posted on March 1, 2011

- UBM acquires Publishing Expo tradeshow for £320,000 Posted on November 11, 2010

- UBM acquires Lead in Research for £1.45m Posted on November 2, 2010

- UBM acquires Hors Antenne for up to €9m Posted on October 20, 2010

- UBM acquires OBGYN.net for $0.8 million Posted on October 15, 2010

- UBM to acquire 65% stake in Rotaforte International Trade Fairs & Media Posted on October 14, 2010

- UBM acquires Canon Communications LLC for $287 million Posted on September 16, 2010

- UBM agrees to acquire UM Paper for up to $880,000 Posted on September 16, 2010

- UBM Studios acquires virtual recruitment fairs business Astound Posted on September 1, 2010

- UBM Aviation acquires The Route Development Group Posted on August 13, 2010

- UBM acquires Children-Baby-Maternity Products Expo in China and related assets Posted on August 13, 2010

- PR Newswire acquires CORPORATE360 Posted on June 29, 2010

- UBM to acquire majority stake in Navalshore Posted on June 15, 2010

- UBM Global Trade acquires selected Centradex assets Posted on May 6, 2010

- UBM acquires web-based marketing business SharedVue Posted on April 21, 2010

- UBM TechWeb acquires Game Advertising Online for up to $8million Posted on February 26, 2010

You must be logged in to post a comment.