Daily Mail and General Trust plc has issued a pre-close trading update.

Daily Mail and General Trust plc has issued a pre-close trading update.

Ahead of the year end on 30 September 2013, the statement provides an update on the Group’s progress in the current year.

It covers the eleven month period to the end of August 2013 and includes comments on September.

Summary

- Solid Group revenue performance, up 2% underlying#

- Good revenue growth from B2B operations, up 6% underlying#

- Resilient revenue performance at dmg media, down 2% underlying#

- Active portfolio management; targeted acquisitions and non-core asset disposals

- Share buy back programme of £69 million to date

- Net debt/EBITDA ratio expected to be less than 2.0 at year end

- Full Year guidance unchanged and in line with market expectations

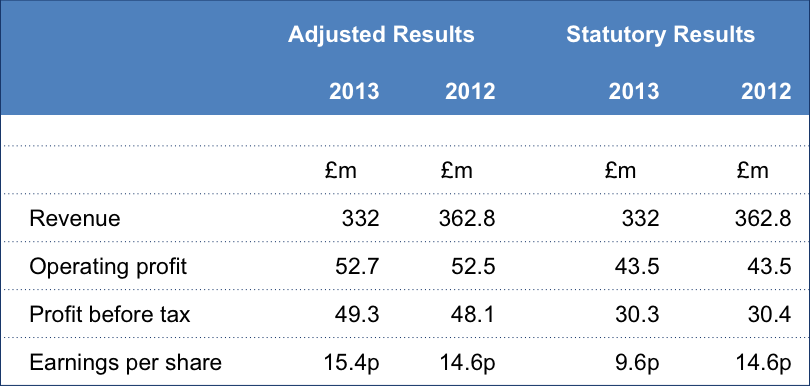

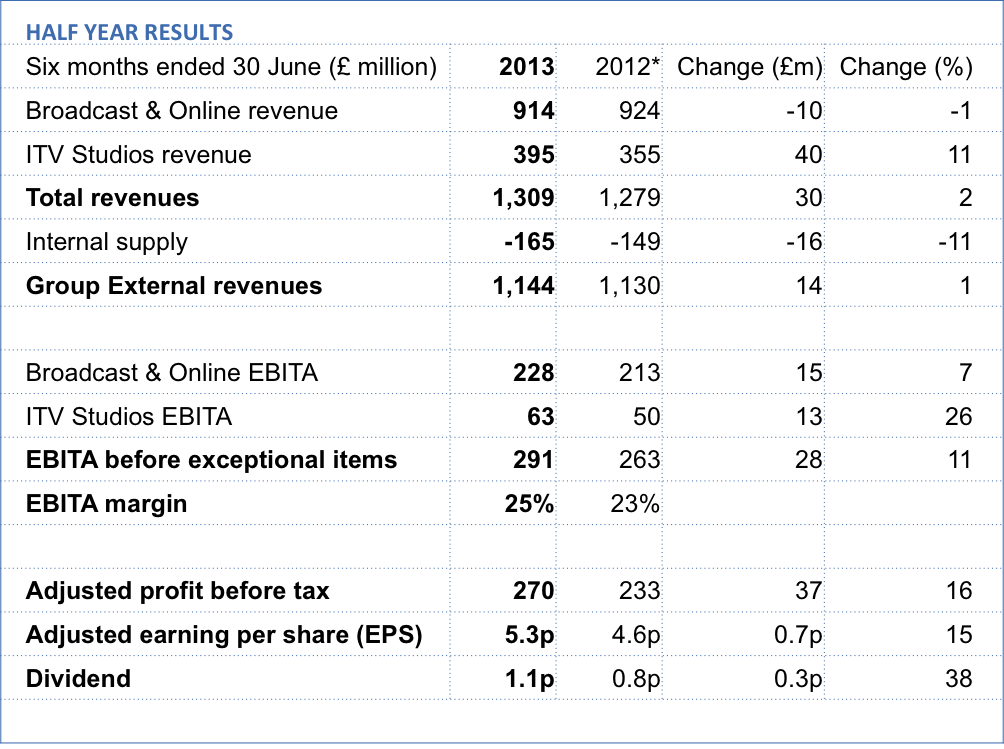

Click on the table for an enlarged view

The full statement can be read here.

UK, London

Related articles:

- DMGT Half Year Preliminary Results Posted on May 23, 2013

- DMGT annual report and M&A update Posted on January 10, 2013

- DMGT has completed its disposal of Northcliffe Media to Local World Posted on January 7, 2013

- Local World to acquire the regional publishing assets of Northcliffe and Iliffe Posted on November 21, 2012

- DMGT sells remaining interest in DMG Radio Australia Posted on September 5, 2012

- DMGT – Q3 results Posted on July 26, 2012

- Acquisition of Xceligentby DMGT Posted on April 27, 2012

- DMGT – trading update for the six-month period to the end of March 2012 Posted on April 17, 2012

- OFT clears the merger between the Digital Property Group and Zoopla Posted onApril 16, 2012

- DMGTacquires Jobrapido Posted on April 16, 2012

- FindaProperty, Primelocation and Zoopla to merge to take on Rightmove Posted onNovember 7, 2011

- DMGT sells GLM to Providence Equity Partners Posted on October 4, 2011

- DMGT trading update September 2011 Posted on September 28, 2011

- DMGT to sell GLM, the United States’ largest privately-held tradeshow management company Posted on June 10, 2011

- DMGT in “informal” talks to buy Express Newspapers Posted on April 4, 2011

- Could DMGT sell Northcliffe? Posted on November 28, 2010

- DMGT back on the acquisition trail? Posted on November 25, 2010

- Associated Northcliffe Digital acquires 50% of Globrix Posted on January 24, 2010

- Associated Northcliffe Digital buys Dothomes.co.uk and Extate.co.uk Posted on February 1, 2010

- Associated Northcliffe Digital acquires 50% of Globrix Posted on January 24, 2010

- Euromoney Institutional Investor – interim management statement to July 24, 2013 Posted on July 26, 2013

- Euromoney Institutional Investor – 6 months results to March 2013 Posted on May 16, 2013

- Euromoney Institutional Investor acquires a majority stake in the Centre for Investor Education in Australia Posted on April 19, 2013

- Euromoney Institutional Investor to acquire HSBC’s Quantitative Techniques operation Posted on April 4, 2013

- Euromoney Institutional Investor acquires Insider Publishing Posted on March 19, 2013

- Euromoney Institutional Investor PLC interim management statement for 4 months to January 30, 2013 February 4, 2013

- Euromoney Institutional Investor PLC acquires Californian conference business TTI/Vanguard January 7, 2013

- Euromoney Institutional Investor Plc announces annual results Posted on November 15, 2012

- Euromoney Institutional Investor PLC – pre-close trading update Posted on September 25, 2012

- Euromoney Institutional Investor PLC – Interim Management Statement for the period from April 1 to July 24, 2012. Posted on July 26, 2012

- Euromoney Institutional Investor – trading update – half year profits of not less than £47M Posted on April 17, 2012

- A Fusion Deal: International grain trading conferences, Global Grain Geneva and Global Grain Asia, sold to Euromoney Institutional Investor Posted on February 29, 2012

- Euromoney Institutional Investor to acquire Ned Davis Research Group for £69M Posted on June 21, 2011

- Euromoney Institutional Investor PLC acquires Arete Consulting Posted on August 13, 2010

- Euromoney sells EIC to Broadfern September 2007

You must be logged in to post a comment.