Daily Mail and General Trust plc (DMGT), commenting on recent media speculation, has announced that it is considering strategic options for its stake in Euromoney Institutional Investor Plc.

Daily Mail and General Trust plc (DMGT), commenting on recent media speculation, has announced that it is considering strategic options for its stake in Euromoney Institutional Investor Plc.

Euromoney is an international business-to-business information company focusing on the global financial community. Holding around 49% of the shares, DMGT is Euromoney’s largest shareholder.

DMGT said it has not received any proposal nor is it in discussions with any party to acquire its holding in Euromoney.

UK, London

Related articles – DMGT

- DMGT to recommend Silver Lake’s recommended cash offer for Zoopla Posted on May 11, 2018

- Zoopla acquires Hometrack for £12M Posted on February 1, 2017

- Zoopla Property group to acquire the Property Software Group Posted on April 20, 2016

- Zoopla Property Group IPO Offer Price Posted on June 18, 2014

- Zoopla Property Group IPO Price Range Posted on June 5, 2014

- Zoopla Property Group Plc – Announcement of Intention to Float on the London Stock Exchange Posted on May 22, 2014

- Zoopla acquires Trinity Mirror property sites Posted on September 5, 2013

- OFT clears the merger between the Digital Property Group and Zoopla Posted on April 16, 2012

- FindaProperty, Primelocation and Zoopla to merge to take on Rightmove Posted on November 7, 2011

- Zoopla acquires Houseprices.co.uk Posted on January 5, 2011

Related Articles – Euromoney Institutional Investor Plc

- Euromoney acquires BoardEx and The Deal for $87.3M Posted on December 7, 2018

- Euromoney acquires price reporting business Random Lengths for $18.2M Posted on August 2, 2018

- Euromoney completes disposal of its Global Markets Intelligence Division (CEIC and EMIS) Posted on May 1, 2018

- Euromoney acquires European investment industry survey Extel Posted on March 8, 2018

- Pageant Media acquires Institutional Investor Journals from Euromoney Posted on January 11, 2018

- Euromoney acquires FastMarkets for £13M Posted on August 15, 2016

- Euromoney sells Gulf Publishing Company and the Petroleum EconomistPosted on April 1, 2016

- Euromoney acquires 10% of Zanbato Posted on September 29, 2015

- Euromoney Institutional Investor completes Dealogic transaction Posted on December 18, 2014

- Euromoney to acquire a strategic shareholding in Dealogic: Sells Capital DATA and Capital NET Posted on November 5, 2014

- Euromoney acquires Investing in African Mining Indaba for £45.3M Posted on July 16, 2014

- Euromoney Institutional Investor acquires Infrastructure Journal for £12.5M Posted on October 15, 2013

- Euromoney Institutional Investor completes acquisition of HSBC’s Quantitative Techniques operation Posted on October 2, 2013

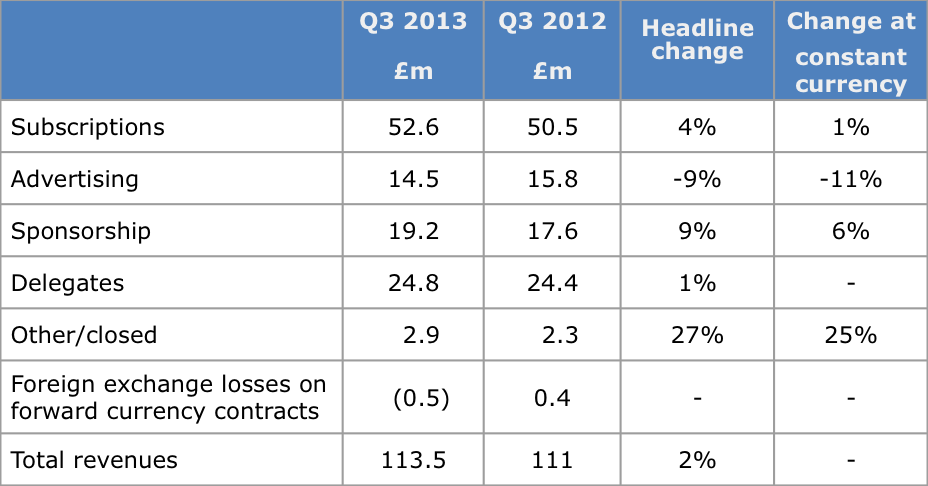

- Euromoney revenues for the fourth quarter increase by 9% Posted on September 24, 2013

- Euromoney Institutional Investor – interim management statement to July 24, 2013 Posted on July 26, 2013

- Euromoney Institutional Investor – 6 months results to March 2013 Posted on May 16, 2013

- Euromoney Institutional Investor acquires a majority stake in the Centre for Investor Education in Australia Posted on April 19, 2013

- Euromoney Institutional Investor to acquire HSBC’s Quantitative Techniques operation Posted on April 4, 2013

- Euromoney Institutional Investor acquires Insider Publishing Posted on March 19, 2013

- Euromoney Institutional Investor PLC interim management statement for 4 months to January 30, 2013 Posted on February 4, 2013

- Euromoney Institutional Investor PLC acquires Californian conference business TTI/Vanguard Posted on January 7, 2013

- Euromoney Institutional Investor Plc announces annual results Posted on November 15, 2012

- Euromoney Institutional Investor PLC – pre-close trading update Posted on September 25, 2012

- Euromoney Institutional Investor PLC – Interim Management Statement for the period from April 1 to July 24, 2012. Posted on July 26, 2012

- Euromoney Institutional Investor – trading update – half year profits of not less than £47M Posted on April 17, 2012

- A Fusion Deal: International grain trading conferences, Global Grain Geneva and Global Grain Asia, sold to Euromoney Institutional InvestorPosted on February 29, 2012

- Euromoney Institutional Investor to acquire Ned Davis Research Group for £69M Posted on June 21, 2011

- Euromoney Institutional Investor PLC acquires Arete Consulting Posted on August 13, 2010

- Euromoney sells EIC to Broadfern Posted September 2007

You must be logged in to post a comment.